{kind=link}

Picture supply: Getty Photos

It’s a easy indisputable fact that Brits aren’t setting apart sufficient cash to assist them fund their retirement. The rising value of dwelling means the quantity we’ve got to save lots of or make investments — equivalent to by shopping for UK development and dividend shares — is on the decline.

Scottish Widows’ newest annual ‘Retirement Report’ underlines the dimensions of the issue. After interviewing 5,072 UK adults, the pensions big mentioned that “38% of individuals are actually on monitor for dwelling requirements in retirement under the minimal stage“.

That’s 3% larger than 2023’s survey. To place that in perspective, it means an additional 1.2m persons are on target to get pleasure from a sub-minimum lifestyle after they retire.

Right here’s my plan

So what would life like appear to be below this life commonplace class? Scottish Widows’ has used the Pensions and Lifetime Financial savings Affiliation’s (PLSA) definition of the minimal dwelling commonplace, which for a single individual permits for:

- £50 per week for groceries, and £25 a month for consuming out

- No automotive, and £10 per week for taxis and £100 a yr for trains

- Every week-long UK vacation every year

- A primary TV and broadband package deal

- £630 a yr to spend on clothes and footwear

To me, it is a fairly chilling prospect. I don’t plan to spend most of my life working solely to then stay on the breadline after I finally retire. I’m positive you are feeling the identical!

So I make investments as a lot as I can each month to try to construct a wholesome nest egg for retirement, even throughout this cost-of-living disaster. The sooner all of us start our journey, the higher.

However I consider that high-yield dividend shares — just like the one described under — might assist even those that start investing later in life to get pleasure from a snug retirement.

7.2% dividend yield

Aviva (LSE:AV.) has one of many largest ahead dividend yields on the FTSE 100 immediately. At 7.2%, it’s double the index common of three.6%.

Monetary companies companies could be susceptible throughout financial downturns when client spending falls. However because of its formidable money reserves, Aviva seems in good condition to proceed paying massive dividends for the foreseeable future.

Its Solvency II capital ratio was a formidable 206% as of March. This even allowed the enterprise to purchase again a whopping £300m of its shares earlier this yr.

I’m assured Aviva may have the means to steadily develop dividends over time, too. Demand for its pensions, financial savings, and safety merchandise ought to rise significantly because of beneficial demographic adjustments.

A £30k+ passive revenue

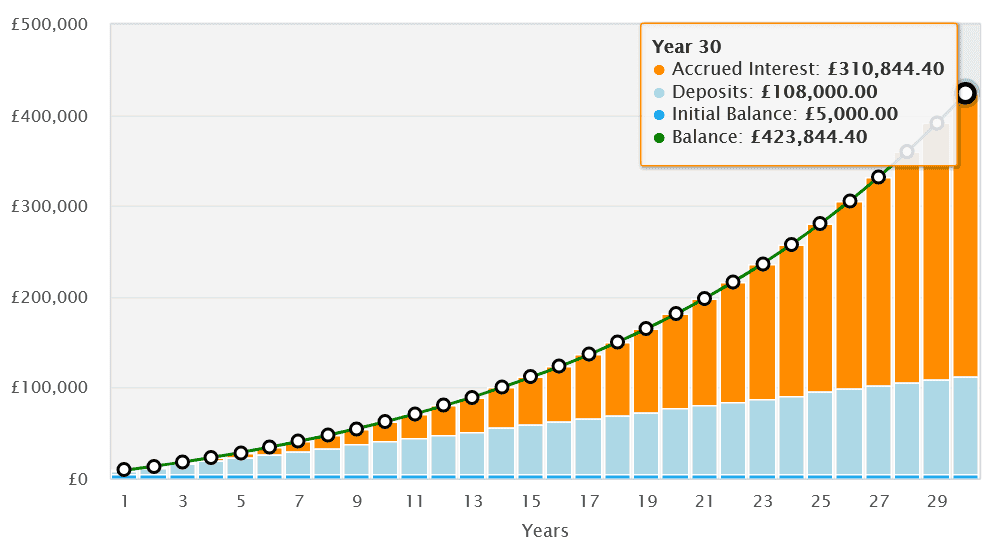

If I had £5,000 to spend money on Aviva shares, I might anticipate to make an annual passive revenue of £360 this yr. That’s primarily based on the corporate’s 7.2% dividend yield for 2024.

If dividends stay the identical together with the share value, my £5k lump sum would flip into £43,077 after 30 years with dividends reinvested. If I supplemented this preliminary funding with an additional £300 a month, I might flip this into £423,844 by 2049.

At this level I’d be incomes an annual passive revenue of £30,517. Mixed with the State Pension, this could possibly be greater than sufficient to permit me to retire in consolation.