{kind=link}

Picture supply: Unilever plc

I actually just like the funding case for Unilever (LSE: ULVR). So too, it appears, do different buyers. The Unilever share value has surged 23% this yr.

For a long-established blue-chip agency in a mature business promoting on a regular basis staples, that looks as if a giant soar.

Why I just like the funding case

To start out, let me clarify why I just like the Unilever funding case usually.

It operates in an space that’s more likely to see excessive and sustained demand for many years (dare I say, even perhaps centuries) to return. Shampoo and laundry detergent might not be thrilling enterprise areas, however I don’t see them going away any time quickly.

Such markets have a tendency to draw a horde of firms eager for a slice of the pie. By spending many years investing in build up premium manufacturers akin to Dove and Marmite, Unilever has helped set itself aside from the group.

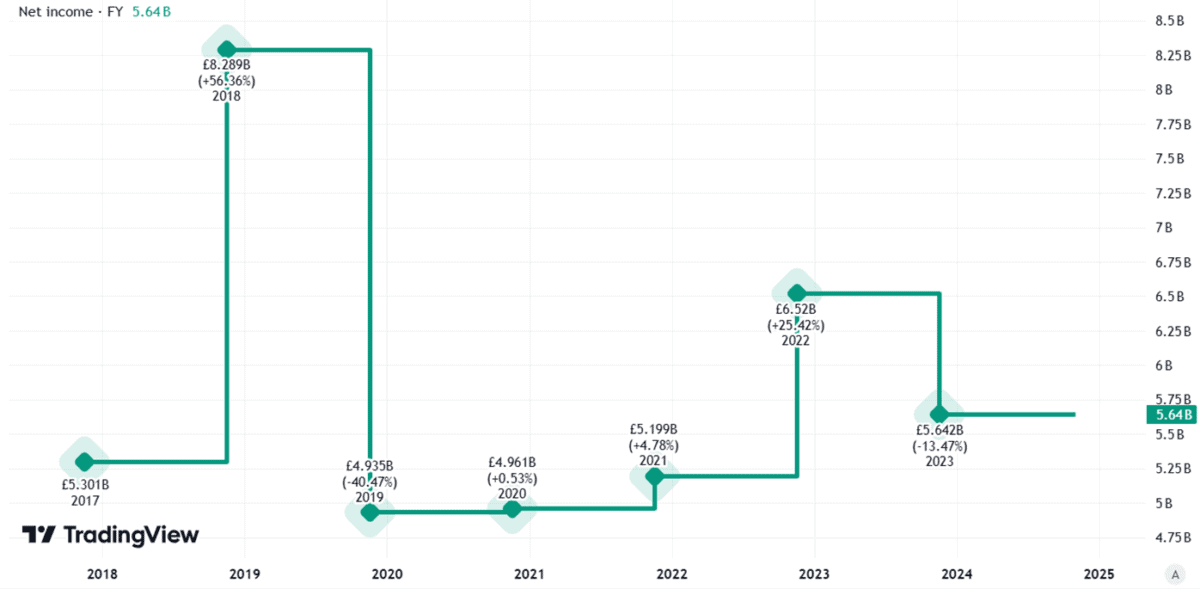

That offers it pricing energy, which in turns helps generate income. Sure, the corporate’s income have moved about lately. However they’ve constantly been within the billions of kilos.

Created utilizing TradingView

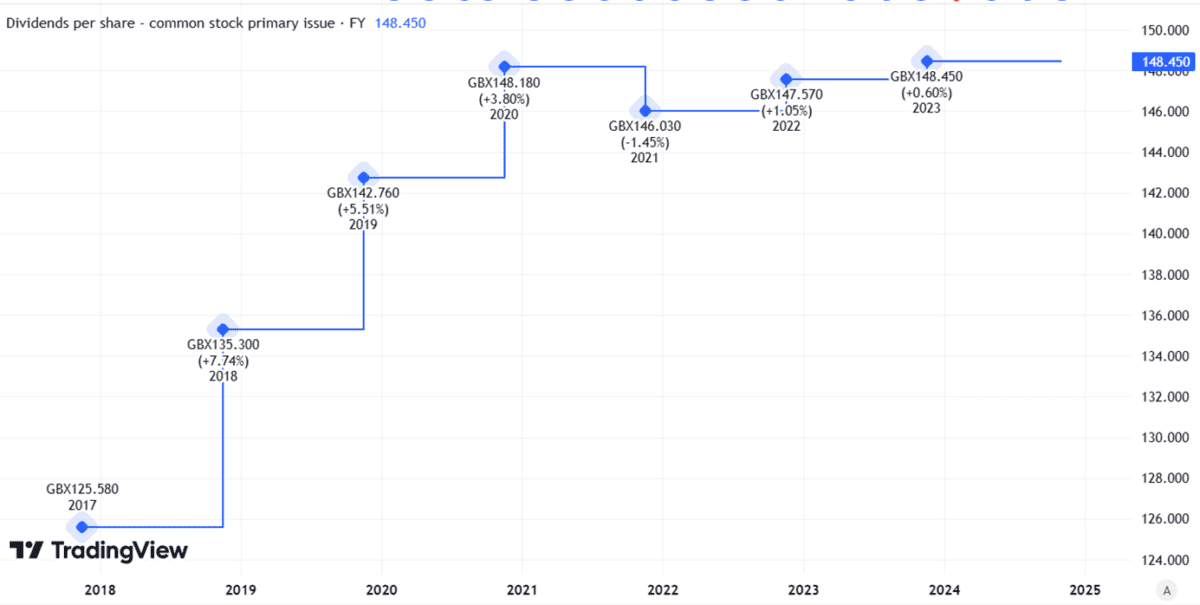

In flip, that helps fund dividends.

Created utilizing TradingView

Revisiting Warren Buffett’s takeover try

Is it a coincidence, then, that Warren Buffett tried to purchase Unilever – not some shares in it, however the entire caboodle – in 2017?

I might say by no means.

Unilever has all of the hallmarks of a traditional Buffett funding: a big, enduring market, sturdy aggressive benefit and confirmed money technology potential.

Understanding latest value strikes

Buffett failed. That was at £40 per share. However, within the years since, the Unilever share value has repeatedly traded beneath (in actual fact, nicely beneath) that value.

So, why has it surged this yr?

New administration may very well be a part of the reason. Plans to chop headcount on the large multinational dangle the prospect of decrease prices, doubtlessly boosting revenue margins.

So too may a plan to spin off the ice cream enterprise and concentrate on areas like private magnificence, with its enticing margins and no want for a difficult refrigerated provide chain from Cornetto manufacturing unit to nook store.

An investor occasion final week confirmed that it’s on observe to ship on its cost-cutting objectives and the agency additionally elaborated on its “Development Motion Plan 2030”. The corporate mentioned it’s on observe to separate its ice cream enterprise from the remainder of the agency by the tip of subsequent yr.

Not liking the share value

Nonetheless, that seems like pretty sluggish progress to me. It means that patrons on the proper value might not have been chomping on the bit (or on the Ben & Jerry’s).

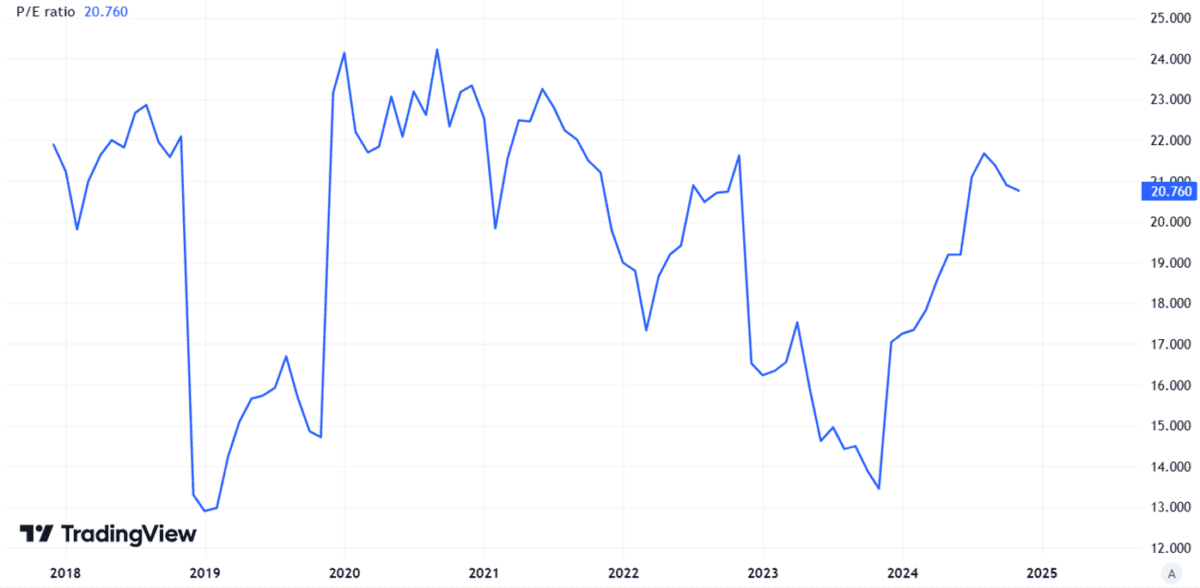

In the meantime, progress plans are all nicely and good (although might be arduous to ship in such a mature enterprise) however based mostly on present efficiency, the Unilever share price-to-earnings ratio is already 21.

Created utilizing TradingView

I don’t assume that’s outrageous, however it’s larger than I’m comfy with as a potential investor, though I just like the Unilever funding case.

The corporate faces dangers, from promoting the ice cream enterprise at too low a value simply to do away with it, to a weak financial system pushing down demand for branded merchandise. So for now, I’ve no plans so as to add Unilever to my portfolio.