{kind=link}

Picture supply: Getty Photos

Greggs (LSE: GRG) shares have smashed it because the pandemic. I don’t maintain the excessive avenue bakery chain in my portfolio, however I want I did. Now I’m questioning if it’s the suitable time to purchase.

The Greggs share worth has soared by 47.1% within the final two years. The inventory would have turned a £10,000 funding into £14,710. With dividends, the full can be nearer to £15,500.

In fact, with hindsight we would all be millionaires. Recently, Greggs shares have slowed. They’re up simply 2.93% during the last 12 months. Over the identical interval, the FTSE 250 as an entire grew 5.72%.

Traders love Greggs, judging by the visitors on our website, however there’s a difficulty right here. Perhaps they adore it somewhat an excessive amount of.

FTSE 250 development inventory

There’s actually lots to love. 2023 noticed “one other yr of fast development and robust progress”, within the phrases of CEO Roisin Currie. Complete gross sales jumped 19.6% to £1.81bn, as Greggs expanded its community of shops past 3,000. It additionally offered extra per retailer, with like-for-like gross sales up a tasty 13.7%. Pre-tax earnings jumped 13% to £167.7m.

In October 2021, it introduced formidable plan to double gross sales inside 5 years and it has made a robust begin. If it disappoints, the backlash might be brutal, which brings me to that difficulty I discussed.

The shares are a bit costly. Buying and selling at 22.34 instances earnings they’re 70% increased than the FTSE 250 common of 13.1 instances. Markets have priced a whole lot of development in there. If it doesn’t come by way of, the share worth may take a success.

I’m fairly optimistic about Greggs’ prospects. It’s a excessive avenue fixture now. It survived pandemic lockdowns and has thrived throughout the cost-of-living disaster. As a purveyor of low-cost treats, it might need benefited as consumers traded down.

The shares may do even higher when folks have a bit additional cash to spend. Though there’s a hazard they may commerce as much as one thing pricier as a substitute.

It additionally pays dividends

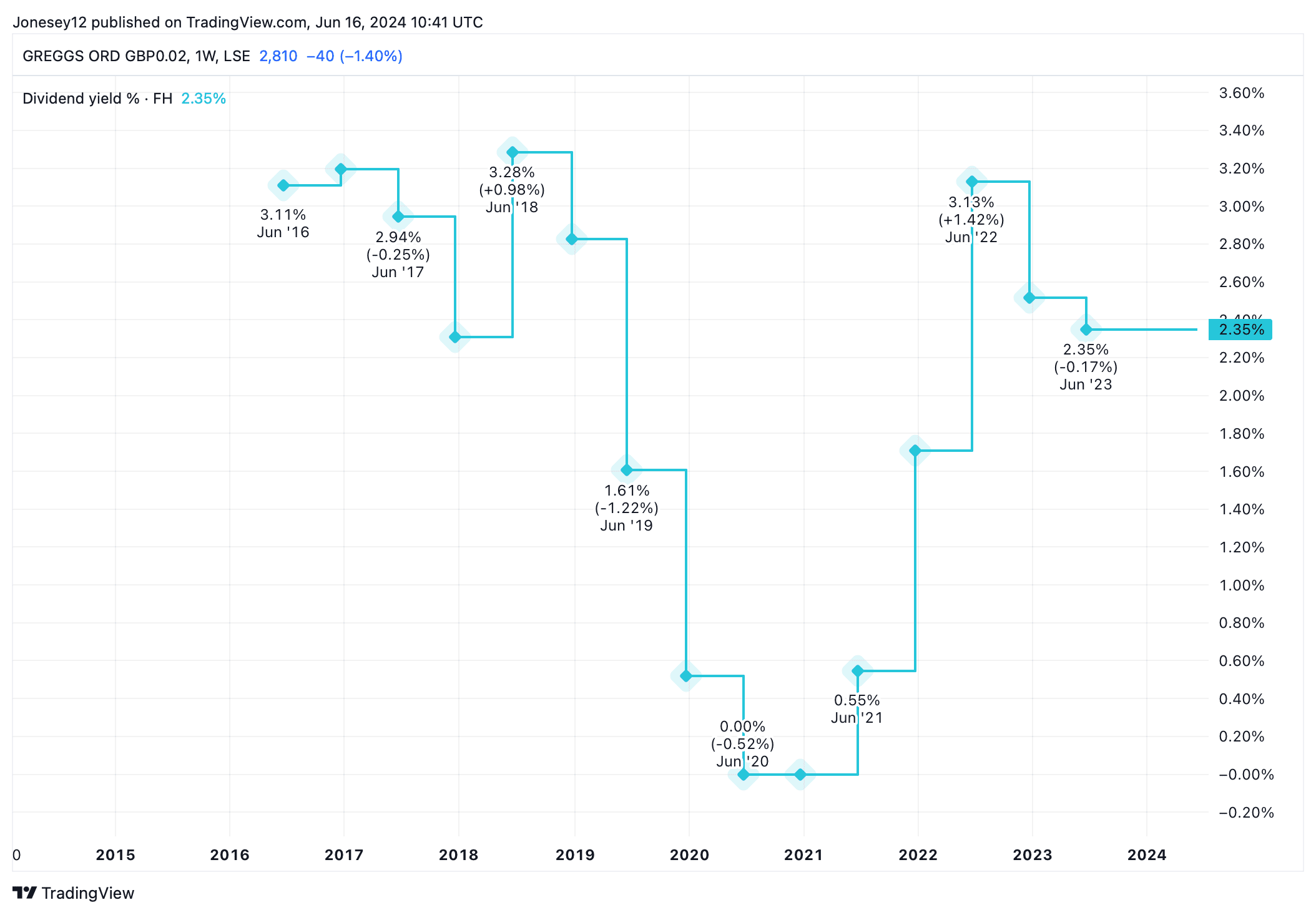

Greggs isn’t nearly development. It pays dividends too. Whereas the yield is simply 2.21% the board has labored laborious to reward shareholders after being pressured to drop shareholder payouts throughout the pandemic. Right here’s what the charts say.

Chart by TradingView

The board elevated the 2023 dividend by 5% from 59p to 62p per shares, and paid a particular dividend of 40p on prime. It may simply afford that, with internet money from working actions after lease funds up 29% to £257m.

But I don’t assume it’s the suitable time for me to purchase Greggs immediately. That prime valuation appears to counsel that its shares have gone so far as they will for now. They’ve been idling since full-year outcomes had been revealed in March. Traders could have gotten somewhat bit too carried away.

There’s additionally the underlying danger that every one these messages about wholesome consuming and processed meals lastly get by way of. Greggs’ ironic cult standing could now be priced into its valuation. However what if consumers resolve the joke isn’t humorous anymore? I wouldn’t need to be holding the shares if tastes change, and received’t purchase it. I can discover higher worth on the FTSE 250 immediately.