{kind=link}

Picture supply: Getty Pictures

Is funding about timing? It’s not solely about timing after all, however timing could be essential. The identical share could be a sensible performer or a complete canine for an investor, relying on after they purchase or sells it. So when in search of shares to purchase, I take into account how engaging the enterprise is – but in addition at what level I’d be completely happy to speculate.

Listed below are two shares on my watchlist that I believe are glorious companies. I’d be completely happy to purchase shares subsequent 12 months if their worth comes right down to what I see as a horny degree.

Dunelm

At face degree, Dunelm (LSE: DNLM) won’t even appear costly. In spite of everything, its price-to-earnings ratio of 14 is decrease than that of some shares I purchased this 12 months, resembling Diageo.

Nonetheless, I’ve been burnt proudly owning retailers’ shares earlier than (resembling my stake in boohoo).

Retail tends to be a reasonably low revenue margin enterprise, so earnings can fall considerably for comparatively small seeming causes. Final 12 months, for instance, Diageo’s after tax revenue margin was 19%. Dunelm’s was lower than half of that, at 9%.

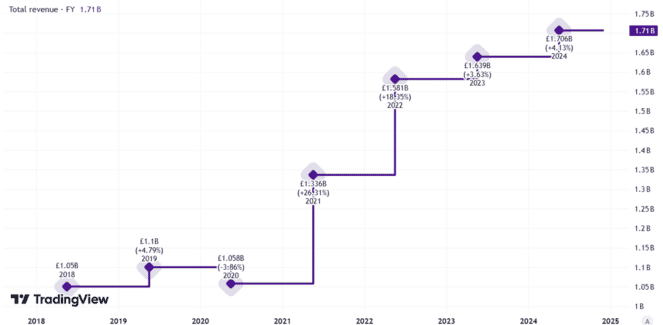

Dunelm’s enterprise is run effectively, it has a big store property, and rising digital footprint and because of many distinctive product traces it might differentiate itself from opponents. Gross sales have grown significantly lately.

Created utilizing TradingVew

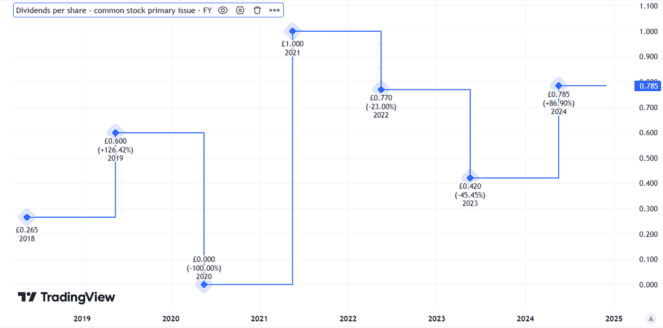

Dunelm is a strong dividend payer too. The yield from unusual dividends is round 4.1%.

However the firm has usually paid particular dividends, that means the whole yield has usually been greater than the unusual dividend yield alone.

Created utilizing TradingVew

Nonetheless, the Dunelm share worth has risen 57% since September 2022.

That appears steep to me provided that gross sales progress in probably the most not too long ago reported quarter was 3.5% — completely respectable in my opinion, however not spectacular.

A weak economic system and more and more stretched family budgets might eat into gross sales and earnings in 2025, I reckon. If that occurs and the share worth falls sufficient, my present plan can be to purchase some Dunelm shares for my portfolio.

Nvidia

I reckon it’s straightforward to take a look at the Nvidia (NASDAQ: NVDA) worth chart and instantly assume “bubble!”

Certainly, the P/E ratio of 53 provides little or no margin of security for dangers resembling a pullback in AI spending as soon as the preliminary spherical of massive installations at present underway has run its course. That helps clarify why I’ve not purchased the shares this 12 months.

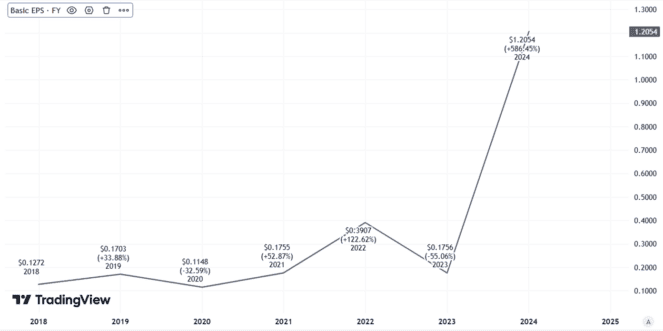

Nonetheless, that P/E ratio is regardless of Nvidia inventory rising 2,175% prior to now 5 years alone. The worth has soared, however so too have earnings.

Created utilizing TradingVew

Nvidia isn’t some meme inventory with out a long-term future. It’s a vastly worthwhile, profitable firm with a confirmed enterprise mannequin.

Its aggressive moat can be large in my opinion – rivals merely can’t make lots of the chips Nvidia does even when they wish to.

The valuation alone is why I’ve not purchased Nvidia inventory this 12 months. It’s a share I’d be completely happy to purchase (in spades) in 2025 if the value seems extra affordable to me.